Atradius Atrium

Nowy portal internetowy zapewniający bezpośredni dostęp do informacji dot. polisy, limitów kredytowych jak również do Atradius Insights i Collect@Net.

Polska

Polska

Australia

Australia

Austria

Austria

Belgia

Belgia

Brazil

Brazil

Bułgaria

Bułgaria

Chiny

Chiny

Czechy

Czechy

Dania

Dania

Finlandia

Finlandia

Francja

Francja

Grecja

Grecja

Holandia

Holandia

Hongkong

Hongkong

Indie

Indie

Irlandia

Irlandia

Japonia

Japonia

Kanada

Kanada

Litwa

Litwa

Meksyk

Meksyk

Niemcy

Niemcy

Norwegia

Norwegia

Nowy Zelandia

Polska

Nowy Zelandia

Polska

Portugal

Portugal

Rumunia

Rumunia

Singapur

Singapur

Słowacja

Słowacja

Słowenia

Słowenia

Spain

Spain

Stany Zjednoczone

Stany Zjednoczone

Szwajcaria

Szwajcaria

Szwecja

Szwecja

Turcja

Turcja

Węgry

Węgry

Wielka Brytania

Wielka Brytania

Włochy

Włochy

Zjednoczone Emiraty Arabskie

Zjednoczone Emiraty Arabskie

Based on survey responses in the Czech Republic, companies now transact more than half of business-to-business (B2B) sales on credit, the highest share in CEE. Medium-sized firms in services lead this trend, showing the strongest reliance on deferred payments in B2B trade relationships. In line with wider regional trends, this reflects a clear shift towards using credit to support sales and remain competitive, despite an uncertain environment and elevated payment risk.

Payment terms offered by Czech firms are broadly in line with CEE, with most invoices due within 30 days from invoicing. However, Czech companies show a stronger preference for tight payment policies and are less likely to extend longer terms. This reinforces a cautious approach to managing payment cycles, even as credit use expands.

More Czech businesses than in CEE report not significant recent changes in B2B payment behaviour. However, among those observing shifts, deterioration is reported more often and appears stronger. This suggests that underlying liquidity pressures continue to weigh on customer payment performance, even when firms maintain strict payment discipline.

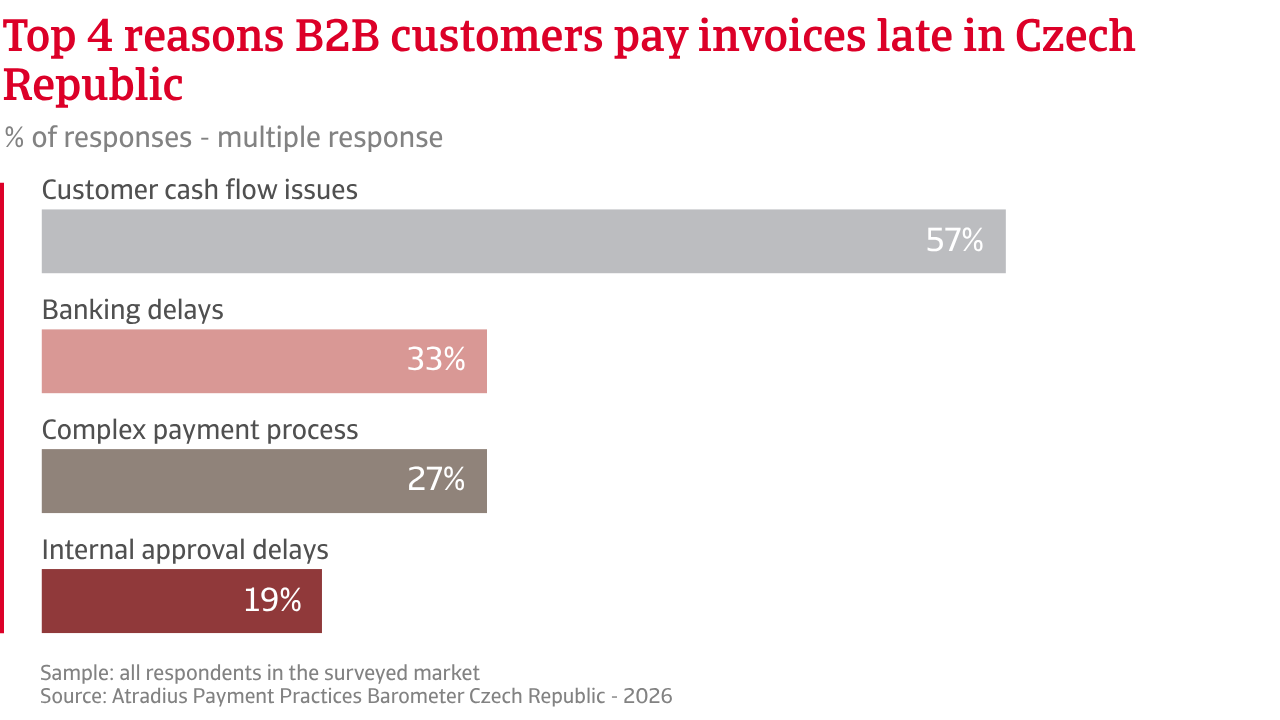

Four in five businesses in the Czech Republic report payment delays from B2B customers, affecting nearly one third of invoices. These metrics are broadly in line with CEE. SMEs in manufacturing are the most exposed. Overdue B2B invoices have increased in recent months, adding pressure on cash flow and raising payment risk. Around three in five firms cite customer liquidity shortages as the main cause, slightly below the regional average. Czech companies also report more operational payment issues, which further disrupt timely collections.

Bad debt write-offs are mainly driven by ageing invoices and customer insolvency, both cited more often than in CEE, particularly by large trade firms. A higher share of Czech companies report losses in the 2% to 5% range, indicating that risk is more concentrated rather than widespread across the customer base.

While liquidity constraints are clear, the impact is managed differently than in CEE. Czech companies are less likely to rely on external financing or delay payments to suppliers, reducing the risk of knock-on effects along the supply chain. Instead, they report tighter financial flexibility and constraints on investment, pointing to a longer-term impact on the business. Businesses in CEE, in contrast, report greater reliance on external funding and more frequent cash flow challenges.

Risk mitigation approaches also differ. Czech companies rely less on active credit management tools such as adjusting terms or offering incentives. Instead, they focus on selective measures, including customer diversification and internal buffers. Across CEE, firms adopt a broader set of tools, including wider use of credit insurance, reflecting a more active response to higher payment uncertainty.

Czech companies now transact more than half of B2B sales on credit, the highest share in CEE. Medium-sized firms in services lead this trend, showing the strongest reliance on deferred payments in B2B trade relationships.

Most Czech businesses do not expect significant short-term changes in B2B payment behaviour, and the share of businesses holding this view is notably higher than in CEE. Among those anticipating shifts, expectations remain cautious, with companies pointing to only gradual and uneven improvements rather than a broad recovery, reflecting ongoing liquidity constraints and persistent payment risk.

Insolvency expectations are consistent with this outlook. More Czech companies than their peers in CEE believe insolvency levels will remain at current elevated levels, while fewer expect a further increase in the short term. At the same time, a meaningful share of businesses express no clear view, highlighting some uncertainty about the short-term economic outlook.

Profit margin expectations are slightly more positive than in CEE, suggesting greater confidence in preserving profitability despite continued cost and financing pressures. Czech firms also show lower concern about macroeconomic risks, including inflation and economic slowdown, pointing to stronger confidence in domestic conditions.

Czech companies also show relatively lower concern about broad macroeconomic risks. Fewer firms cite economic slowdown or inflation as key threats compared with CEE, while geopolitical risk is also less prominent. This points to stronger confidence in domestic conditions and resilience at market level. Financial risks follow a similar pattern. Concerns about interest rates and currency volatility remain broadly in line with CEE, but are slightly less acute, indicating no major divergence in funding pressures.

In contrast, Czech firms place greater emphasis on operational risks. Cybersecurity and fraud are cited more frequently than in CEE, alongside higher concern about sector specific downturns and supply chain disruption. This highlights a more focused and granular risk perspective, where attention shifts from broad macroeconomic pressures to business specific vulnerabilities and operational resilience.

For a full overview of the 2026 survey results for the Czech Republic, please download the market specific report from the related documents section below. Insights into Central and Eastern Europe (CEE) are available in the related content section below.

To explore how to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.

Prośba o oddzwonienie

Nota prawna