Atradius Atrium

Nowy portal internetowy zapewniający bezpośredni dostęp do informacji dot. polisy, limitów kredytowych jak również do Atradius Insights i Collect@Net.

Polska

Polska

Australia

Australia

Austria

Austria

Belgia

Belgia

Brazil

Brazil

Bułgaria

Bułgaria

Chiny

Chiny

Czechy

Czechy

Dania

Dania

Finlandia

Finlandia

Francja

Francja

Grecja

Grecja

Holandia

Holandia

Hongkong

Hongkong

Indie

Indie

Irlandia

Irlandia

Japonia

Japonia

Kanada

Kanada

Litwa

Litwa

Meksyk

Meksyk

Niemcy

Niemcy

Norwegia

Norwegia

Nowy Zelandia

Polska

Nowy Zelandia

Polska

Portugal

Portugal

Rumunia

Rumunia

Singapur

Singapur

Słowacja

Słowacja

Słowenia

Słowenia

Spain

Spain

Stany Zjednoczone

Stany Zjednoczone

Szwajcaria

Szwajcaria

Szwecja

Szwecja

Turcja

Turcja

Węgry

Węgry

Wielka Brytania

Wielka Brytania

Włochy

Włochy

Zjednoczone Emiraty Arabskie

Zjednoczone Emiraty Arabskie

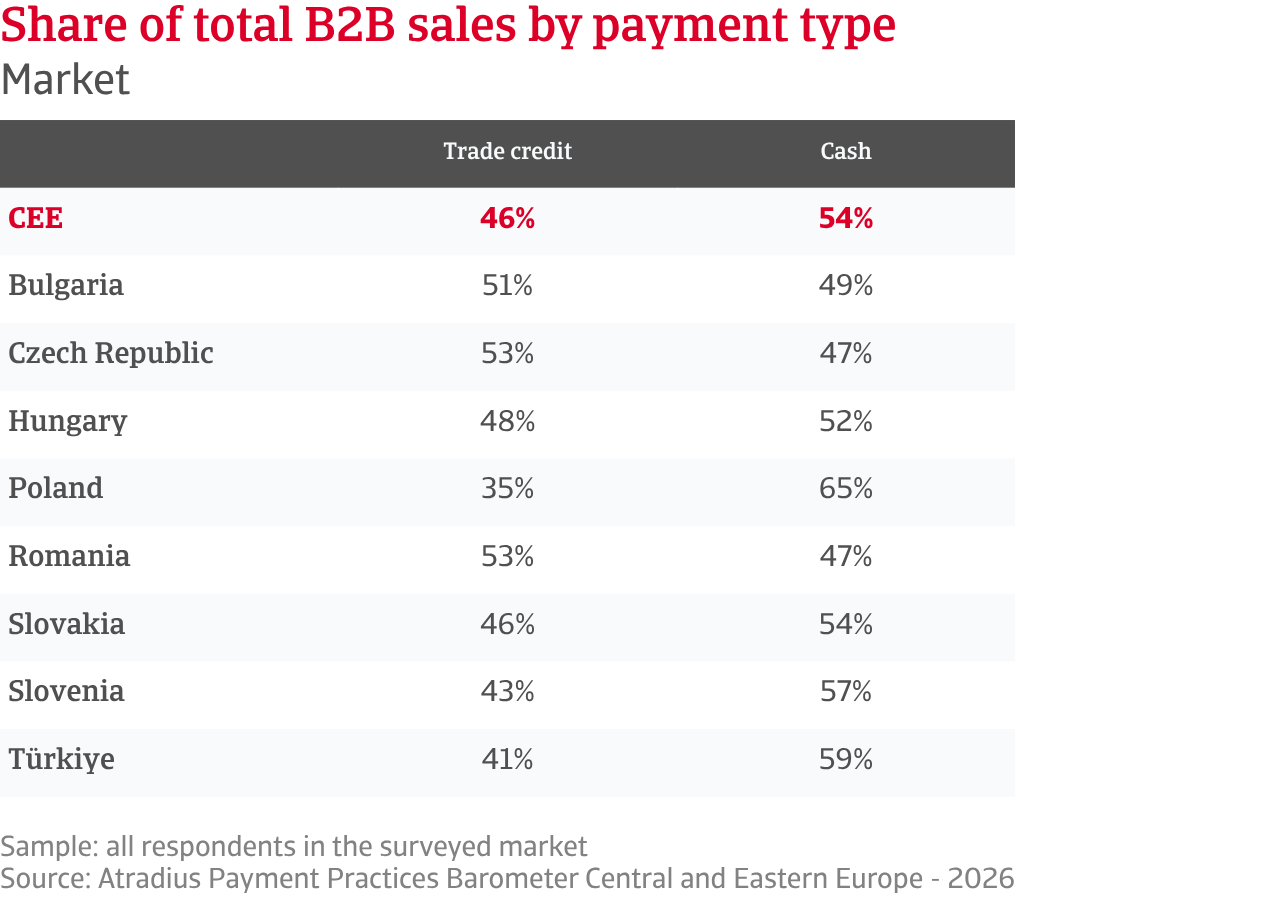

Across Central and Eastern Europe (CEE), companies appear to favour cash in business-to-business (B2B) trade. This reflects a clear focus on protecting liquidity in an environment where payment risk remains high. With 54% of transactions settled at the point of sale, payment certainty continues to outweigh the use of trade credit in B2B commercial relationships. However, the remaining 46% of sales still take place on credit, confirming that allowing business customers to defer payment for goods or services under agreed payment terms remains essential in CEE intercompany trade, even as suppliers manage it more cautiously. Differences across sectors and markets are clear. SMEs in services are the most likely to sell on credit, while companies in the Czech Republic and Romania make the greatest use of trade credit across the region. Bulgaria and Hungary follow, while Slovakia aligns closely with the regional average. By contrast, Slovenia and Türkiye rely less on trade credit, with Poland recording the lowest use overall.

Despite this preference for cash, trade credit is gaining ground. Companies are extending credit to sustain sales and support customers facing liquidity pressure. Manufacturing and larger firms are leading this shift, reflecting their role in complex supply chains and international trade. Smaller services firms, although reliant on credit themselves, remain more cautious, with tighter cash positions limiting how far they can extend it. At country level, this expansion is most evident in Slovakia, Türkiye, and the Czech Republic, while Hungary and Bulgaria show more restraint. Romania remains a key user, but signs point to a more cautious approach.

.2026-06-10-14-53-43.png)

Most CEE suppliers still operate with short payment cycles. Terms within 30 days from invoicing remain the norm across the region, with longer terms used selectively to support competitiveness. Even where credit is extended, companies prioritise keeping cash inflows quick and reliable. Medium-sized and larger firms tend to offer more flexibility, supported by some improvements in payment behaviour among business customers. Smaller firms, particularly in services, remain more cautious, as they have less room to absorb shocks. At market level, Türkiye stands out for the most relaxed payment terms, combined with the highest share of businesses saying customer payment behaviour has weakened. Romania shows a similar picture, although with shorter terms, suggesting that strict policies alone do not fully protect suppliers. Elsewhere in the region, B2B payment behaviour shows limited improvement, but it remains inconsistent. This helps explain why most companies continue to favour short payment cycles, especially in Bulgaria, while Hungary remains the most cautious.

.2026-06-09-16-04-04.png)

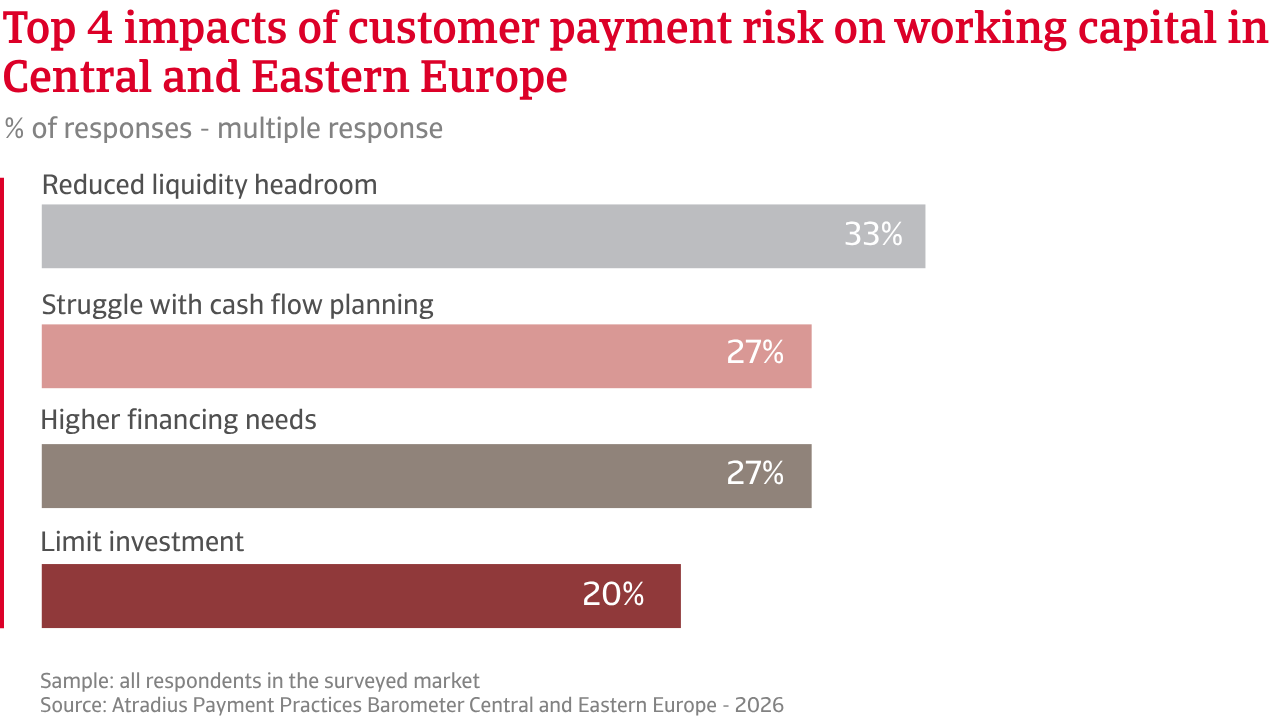

Against this backdrop, late payments remain widespread. Around 83% of CEE suppliers report delays, with nearly one third of invoices overdue. The impact on working capital is significant, forcing companies to rely on reserves or external financing. Manufacturing and medium sized firms are the most affected, while services companies appear less exposed, likely due to faster cash cycles and smaller transactions. By market, late payments are most pronounced in Türkiye and Slovakia, followed by Slovenia and Romania, while Hungary reports the lowest levels.

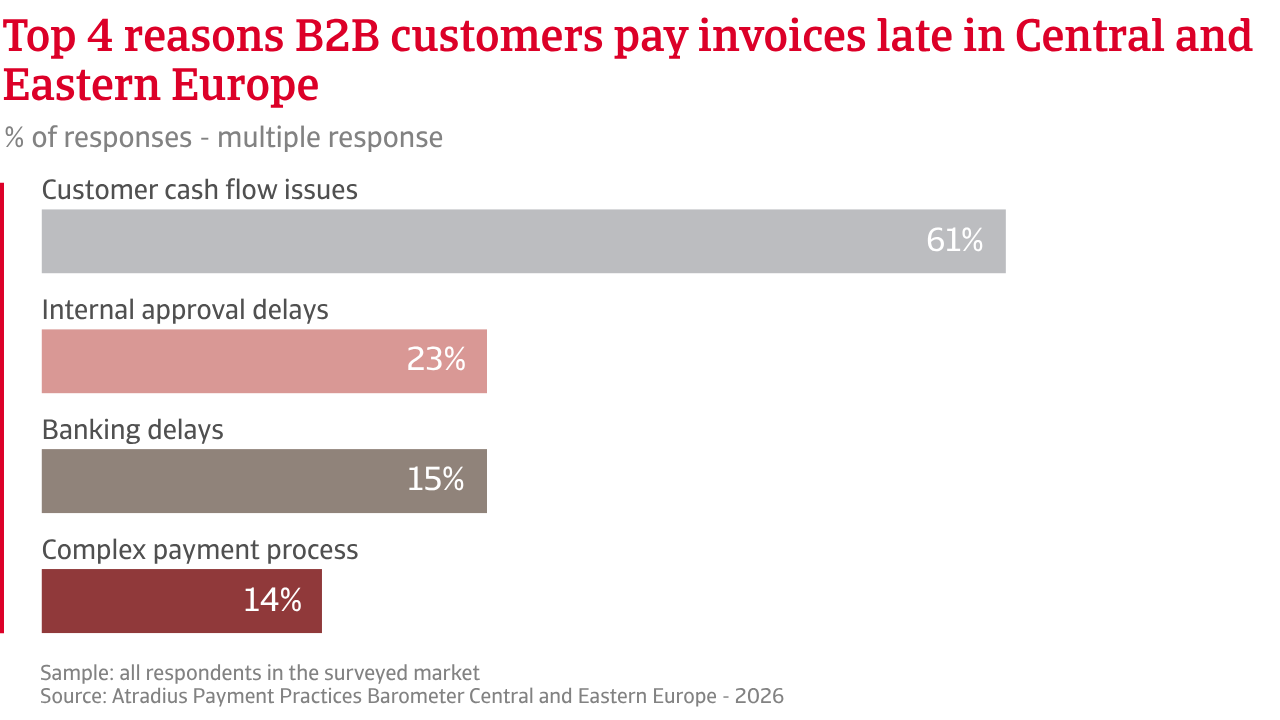

The drivers of delay are clear. Around six in ten companies cite customer liquidity pressure as the main cause, particularly among large manufacturers and firms in Türkiye and Bulgaria. Operational factors also play a role, with around one in four companies pointing to banking processes, especially in Romania and the Czech Republic.

Looking at payment timing, reflected in Days Sales Outstanding (DSO) data, survey evidence shows that more payments are drifting into delay, increasing the amount of working capital tied up in receivables and not available for operations. This increases financial pressure on the business, as well as the likelihood of missed payments. More CEE companies now report rising write-offs than declines, indicating that part of this delayed flow is already turning into losses. The age of receivables remains the main trigger for write-offs, confirming that longer delays are key in driving losses. Data by business segment and market highlight that medium to large companies, particularly in manufacturing and trade, and businesses in Türkiye, Romania and Slovakia are the most affected.

The impact on operations is direct and widespread. Delayed payments constrain liquidity, making it harder for companies to plan and manage cash flow. This pressure is most evident among SMEs in services and firms in Türkiye. At the same time, reliance on external financing is increasing, particularly among manufacturing SMEs and companies in Slovakia. Reduced cash availability is also limiting day to day operations, especially for smaller firms and businesses in Slovenia.

To mitigate the impact of customer payment risk on the business, CEE companies are adapting their strategies. The majority are reducing exposure by favouring cash transactions or requesting advance payments, particularly in trade and in Türkiye. Almost as often, companies report setting up internal reserves to absorb losses, a strategy most widespread among manufacturing SMEs and firms in Slovakia. However, more structured risk management tools remain underused. Credit insurance and similar solutions are still relatively limited, although adoption is higher among medium sized firms in trade and companies in Slovenia, where these tools are used to monitor risk and act early.

Overall, the picture is one of growing tension, pointing to rising liquidity stress for businesses across the region, which is becoming a concern for companies selling on credit in B2B trade.

Around 83% of CEE suppliers report delays, with nearly one third of invoices overdue. The impact on working capital is significant, forcing companies to rely on reserves or external financing.

Looking ahead over the year, the outlook for B2B payment behaviour across CEE does not point to a marked shift from current challenging conditions. This reflects a broader economic backdrop marked by uneven growth, persistent cost pressures, tighter financial conditions and ongoing global uncertainty. Together, these factors continue to weigh on business confidence and limit the scope for improvement in customer payment behaviour.

Differences in sentiment across sectors and markets are marked. Manufacturing and services firms, along with smaller businesses, appear slightly more optimistic. This may reflect stronger links to domestic demand and, in some cases, greater flexibility in adapting to changing conditions. By contrast, trade companies stand out as the most pessimistic across the region. Their exposure to demand volatility remains high, inventory cycles and supply chain uncertainty continues to shape a more cautious outlook. Medium and large firms are also more guarded in their expectations, likely reflecting broader exposure across supply chains and customer portfolios. By market, the picture remains fragmented. Slovenia, Türkiye, Bulgaria and Slovakia show some confidence in local economic conditions or recent stabilisation. Hungary stands out for weaker sentiment, reflecting ongoing economic pressure, while the Czech Republic and Romania sit in between, with more balanced but still uncertain expectations. These differences highlight how local economic landscapes continue to shape payment behaviour alongside broader regional trends.

Corporate insolvency risk is emerging as a growing concern across the region. Around 36% of businesses believe insolvency levels will remain at already elevated levels, while an even larger share expects them to rise further in the coming months. The remaining respondents are uncertain. Across sectors, industry and trade show the highest levels of concern, with more than half of companies expecting insolvencies to increase. This reflects their exposure to weaker demand, tighter margins and longer cash conversion cycles. Services, in contrast, show a more balanced view, with fewer businesses anticipating further deterioration, highly likely due to relatively faster cash cycles and closer customer relationships.

Differences by company size are less pronounced, although medium and large firms report slightly higher levels of concern, consistent with their broader exposure and risk profile. Markey level sentiment remains uneven. Businesses in Slovenia, Slovakia and Türkiye report higher levels of concern, while perceptions in the Czech Republic and Hungary are more contained. Overall, insolvency risk is becoming a more prominent concern across CEE, confirming the cautious stance businesses are taking towards trade credit and payment risk.

When asked about the key risks they expect to disrupt B2B payment behaviour in the coming months, companies consistently point to macroeconomic pressures. Concern about economic slowdown and rising cost pressure dominates across sectors, sizes and markets. These factors directly affect customers’ ability to pay and businesses’ willingness to extend credit. Geopolitical uncertainty adds a further layer of risk through trade disruptions, energy costs and supply chain instability, although its impact varies across the region.

Manufacturing, construction and services businesses are particularly concerned about domestic economic conditions, while trade firms are more focused on geopolitical developments, given their reliance on cross border flows and supply chains. SMEs feel demand pressure more acutely, while larger firms show broader risk awareness. By market, Poland and Slovenia show highest concern about the economic outlook, while Hungary, Slovakia and the Czech Republic are more focused on cost pressures. In Türkiye, concerns are more widespread across all risk categories, pointing to a more challenging operating environment.

Overall, the outlook for B2B payment behaviour in CEE remains one of concern, with uncertainty around payment trends combining with elevated insolvency risk and ongoing macroeconomic strain. This suggests that vulnerabilities continue, and businesses are preparing for a prolonged period of tight liquidity, with a continued focus on cash flow and payment risk management.

For a full overview of the 2026 survey results for Central and Eastern Europe, please download the regional report and the statistical appendix from the related documents section below.

To explore how to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.

Prośba o oddzwonienie

Nota prawna